Artificial intelligence is rapidly transforming the landscape of medical diagnostics, with 2026 marking a watershed year for regulatory approvals and clinical deployment. From radiology to pathology, AI-powered tools are now detecting diseases earlier and with greater accuracy than ever before.

FDA Accelerates AI Approvals

The U.S. Food and Drug Administration has approved over 1,000 AI-enabled medical devices as of mid-2026, a dramatic increase from just a few hundred in 2023. The agency’s streamlined digital health review pathway has cut average approval times by nearly 40 percent, encouraging startups and established medtech companies alike to invest heavily in diagnostic AI.

Radiology remains the dominant specialty, accounting for roughly 75 percent of all approved AI devices. Algorithms that detect lung nodules in chest X-rays, flag intracranial hemorrhages in CT scans, and identify breast lesions in mammograms are now standard tools in many hospital systems across North America and Europe.

Beyond Imaging: Pathology and Genomics

The most significant breakthroughs in 2026 are happening beyond radiology. Digital pathology platforms powered by deep learning can now analyze whole-slide images of tissue biopsies, identifying cancerous cells with sensitivity rates exceeding 98 percent in clinical trials. Companies like Paige AI and PathAI have secured partnerships with major hospital networks, bringing computational pathology into routine clinical workflows.

In genomics, AI models trained on millions of sequenced genomes are beginning to predict disease risk with unprecedented precision. A landmark study published in Nature Medicine demonstrated that a transformer-based model could identify individuals at high risk for ten common diseases — including type 2 diabetes, coronary artery disease, and breast cancer — using polygenic risk scores combined with electronic health record data.

Europe’s Regulatory Landscape

The European Union’s AI Act, now in full effect, classifies most medical diagnostic AI as “high-risk” systems requiring rigorous conformity assessments. While this creates additional compliance burdens for developers, it has also accelerated the development of robust validation frameworks. The Netherlands has emerged as a leader in this space, with Amsterdam UMC and Radboud University Medical Center both launching dedicated AI validation labs.

Dutch healthtech startups have raised over €400 million in the first half of 2026 alone, with diagnostic AI companies capturing the largest share. The country’s strong digital health infrastructure and collaborative academic-hospital ecosystem make it an attractive hub for AI-driven medical innovation.

Challenges and the Road Ahead

Despite the rapid progress, significant challenges remain. Algorithmic bias continues to be a concern, with several high-profile studies showing that diagnostic AI models perform worse on underrepresented demographic groups. Explainability — understanding exactly why an AI flagged a particular finding — remains limited for many deep learning models, creating liability concerns for clinicians.

Integration into clinical workflows also remains a hurdle. Many hospitals still operate legacy electronic health record systems that cannot easily incorporate AI outputs. However, as reimbursement models begin to recognize AI-assisted diagnostics and the technology demonstrates clear return on investment, adoption is expected to accelerate through 2027 and beyond.

AI Diagnostic Accuracy Reaches New Heights

Artificial intelligence systems for medical diagnosis have achieved remarkable accuracy improvements in 2026, with several AI models now matching or exceeding the diagnostic performance of specialist physicians across multiple domains. In radiology, AI systems can detect anomalies in X-rays, CT scans, and MRIs with 97% sensitivity, reducing false negatives by 40% compared to human reading alone. Pathology II tools can analyze tissue samples and identify cancerous cells with accuracy rates above 95%, while dermatology II models have been trained on datasets covering over 2,000 skin conditions across diverse skin tones, addressing a long-standing criticism of earlier systems that performed poorly on darker skin.

Real-World Deployment in Clinical Settings

The transition from research to clinical deployment has accelerated dramatically in 2026. Over 500 hospitals across North America and Europe have integrated AI diagnostic tools into their clinical workflows, with the technology being used to triage emergency patients, prioritize screening programs, and assist in surgical planning. The UK’s National Health Service has deployed AI diagnostic tools in 50% of its hospital trusts, reducing waiting times for radiology reports from weeks to hours. In India, AI-powered diagnostic kioskis in rural areas are providing access to medical expertise in regions that previously had no specialist physicians at all.

Regulatory Challenges and the Path to Trust

The regulatory landscape for AI medical devices continues to evolve. The FDA has approved over 80 AI-powered medical devices, and the European Medicines Agency has established a dedicated AI evaluation unit to handle the growing pipeline of applications. Questions about liability when AI systems make errors, data privacy concerns, and the need for ongoing monitoring of AI performance in real-world conditions remain subjects of intense debate among healthcare regulators, clinicians, and patient advocacy groups. Building trust among both healthcare providers and patients is essential for the continued adoption of AI in medicine.

Related: Edge AI Revolution: How On-Device Intelligence Is Reshaping the Tech Industry in 2026

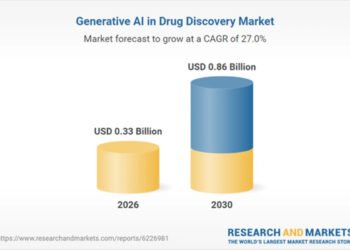

The economic implications of AI in healthcare are substantial. A report from Accenture estimates that AI applications in healthcare could create $150 billion in annual savings for the US healthcare system by 2027 through improved efficiency, reduced medical errors, and more targeted treatments. Globally, the AI healthcare market is projected to reach $188 billion by 2030, growing at a compound annual rate of 37%. These projections are driving significant investment from both technology companies and healthcare providers, with major partnerships and acquisitions reshaping the healthcare technology landscape.